5 Reasons to Never Give Your Children an Outright Inheritance

The Benefits of Structuring Inheritances Strategically

Avoiding Outright Distributions

Planning for the future and the proper management of inheritances are vital considerations for adults. Neglecting these issues often leads to unnecessary conflicts, court battles, and financial burdens associated with probate. Taking charge of your adulthood and making conscious choices about how to leave and receive inheritances can bring healing to your family, honor your ancestral lineage, and serve future generations.

Congratulations on acknowledging the importance of this process. By confronting the reality of death and inheritance, you have already taken a significant step towards consciously creating your life. For parents with young children, setting up a trust for life insurance and investment accounts ensures their financial well-being in the event of premature death. This approach safeguards their assets until the children are mature enough to handle them, ensuring responsible management and allowing you to choose a trusted guardian.

As your children enter their teenage years, you may consider protecting your accumulated wealth from potential risks associated with their age and financial inexperience. Parents often create a nest egg for their children, only to later worry about safeguarding it from their unruly teens and young adults. This concern arises from doubts about their children’s ability to handle significant inheritances without having earned them and uncertainty about their financial support in the parents’ later years.

If your children demonstrate reliability and contribute positively to society during their teenage years, it becomes apparent that they can handle their inheritance. However, if doubts persist, you may conclude that they are not ready or capable of managing the wealth you have built. Now, fluctuations in confidence regarding your children’s abilities are normal. Regardless of the stage you find yourself in, it is crucial to have a well-thought-out plan that avoids potential legal, financial, or tax complications for your legacy.

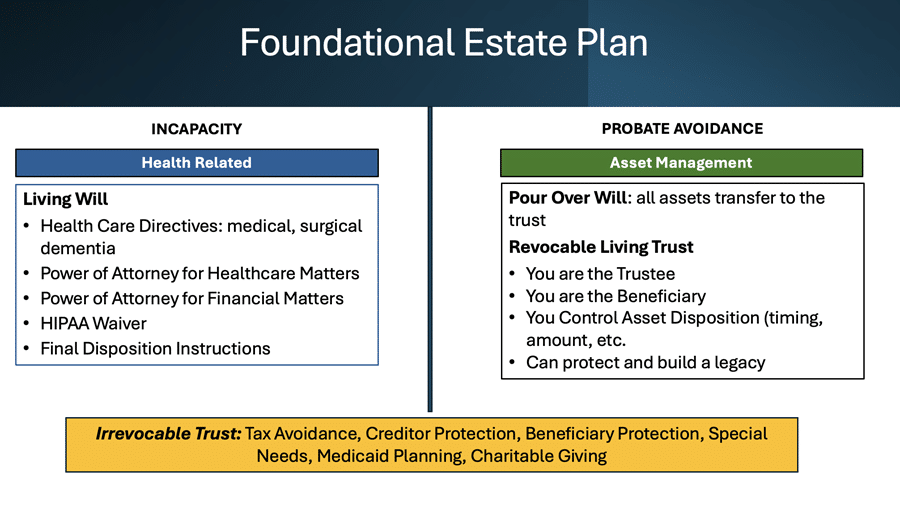

Conventional Estate Planning

Typically, a will or trust drafted by a traditional lawyer stipulates that assets will be held in trust until the children reach a certain age. At that point, the trust terminates, and the assets are distributed outright. However, this is precisely what you want to avoid. If you examine the language in a trust, you will likely come across something similar to the following:

- “For each child of the Grantor who has reached 25 years of age, they shall have the right, through written request, to withdraw one-third of the remaining assets in their share held in trust. For each child who reaches 30 years of age, and each remaining child upon reaching that age, they shall have the right, through written request, to withdraw one-half of the remaining assets in their share held in trust. For each child who reaches 35 years of age, and each remaining child upon reaching that age, they shall have the right, through written request, to withdraw the remaining assets in their share held in trust. If the child exercises this right, the trust as to that share terminates.”

If you encounter such provisions in a trust, it means that when the beneficiary reaches the age of 35, the remaining assets held in the trust are distributed outright into their personal bank account, and the trust terminates. At first glance, this may seem appropriate since, by the age of 35, a beneficiary should possess the maturity to handle inherited assets. However, even if that is the case, distributing the inheritance outright is not the optimal approach.

The Risks Involved

When inherited assets are transferred to a beneficiary’s personal account after the trust terminates, they become susceptible to risks from the beneficiary’s creditors, potential divorces, or lawsuits. Moreover, the beneficiary lacks the incentive to grow the inherited wealth and may choose to spend it rather than create further value. Fortunately, there is a better alternative.

The 5 Common Ways Inheritances Are Lost

Before exploring the better alternative, let’s examine the common ways inheritances are lost:

- Divorce. There is a risk of the loss of inheritance when inherited assets are combined with marital property. For example, if an inheritance is used as a down payment on a shared home, it becomes subject to division upon divorce.

- Financial Mismanagement. Sadly, financial mismanagement is prevalent when beneficiaries lack preparation. Studies show that a significant percentage of inheritors end up spending or losing their entire inheritance due to inadequate financial management skills.

- Extreme debt or bankruptcy. Unforeseen circumstances such as business failures, health issues, or accidents can lead to financial ruin and can result in the complete loss of an outright inheritance.

- Lawsuits. pose a significant threat to inherited wealth. Negligence resulting in harm to others can lead to substantial legal judgments that could wipe out an inheritance left outright to beneficiaries.

- Lost Work Ethic. Unprepared heirs often struggle to handle prosperity. Research suggests that children who receive inheritances may end up with significantly less wealth than those who didn’t, due to excessive spending, identity issues, and guilt over unearned money.

The Better Alternative: the Strategic Approach

The Benefits of a Lifetime Trust

A more effective alternative to outright distributions is the use of a lifetime trust. This type of trust is designed to hold and manage assets for the lifetime of the beneficiaries, offering numerous benefits:

- Asset protection: By keeping the assets within the trust, they are shielded from potential risks such as lawsuits, creditors, or divorces.

- Professional management: Lifetime trusts are typically managed by professional trustees who have experience in investment and financial management. This ensures the assets are properly handled and can grow over time.

- Flexibility in distributions: The trust allows for flexibility in distributing funds to beneficiaries based on specific milestones, such as educational achievements, starting a business, or reaching certain age thresholds. This promotes responsible financial behavior and encourages personal growth.

- Tax efficiency: Lifetime trusts can be structured to minimize tax liabilities, maximizing the value of the inheritance for future generations.

- Preservation of family wealth: By maintaining the assets within the trust, you ensure their preservation for future generations, providing a lasting legacy.

- Mitigation of family conflicts: Clearly defined instructions and guidelines within the trust can help prevent misunderstandings and potential conflicts among family members.

Seeking Professional Advice

To effectively structure inheritances and take advantage of lifetime trusts, it is advisable to consult with an experienced estate planning attorney or a financial advisor who specializes in this area. They can provide personalized guidance based on your specific circumstances, goals, and the applicable legal and tax regulations in your jurisdiction.

In conclusion, by strategically structuring inheritances through the use of lifetime trusts, you can protect assets, promote responsible financial behavior, minimize tax burdens, and preserve your family wealth for future generations. It is a proactive and thoughtful approach that can bring peace of mind and ensure the long-term success of your legacy.