Can A Creditor Take Your Home?

Can A Creditor Take Your Home?

In our heavily litigious society where people sue over practically any real or perceived injury, Colorado and New Mexico passed a “Homestead Exemption” act which exempts a portion of a persons’ homestead from seizure to satisfy a debt, contractual obligation, or civil liability.

That sounds like good news. But is it enough?

In Colorado, the exemption is only up to $250,000 for most individuals or couples and $350,000 for the elderly and disabled. For those living in New Mexico, this Household Exemption is only $150,000 per person. The Homestead Exemption protects only a portion of your home’s equity, leaving a significant amount of your home value vulnerable and at risk.

The Homestead Exemption is applied to the available equity in your home (the value of your home less the amount you own on your mortgage). Given the recent spike in house values in both Colorado and New Mexico, the Homestead Exemption is simply not adequate to protect your home from aggressive litigants.

In addition, the Homestead Exemption DOES NOT apply to your mortgage lender or to any other Secured Creditor. Therefore, if you pledged your home for a debt and default on your loan agreements, a lender can still foreclose.

In short, a creditor (someone who has brought a successful lawsuit against you to collect a debt), can force a sale of your home to collect the amount due them if you cannot otherwise pay the obligation. Yes, they can force you to sell your home, no matter how small the debt.

How Real is the Risk of Being Sued?

Statistics show that every homeowner will likely be sued between 1-3 times during their lifetime. If you are self-employed, run a small business, or a person with significant investment property, you are likely to be sued 2 or 3 times in your lifetime. If you run a bigger business, the numbers rise significantly.

The risk of litigation is real and the

financial exposure is significant!

Can Your Home Be Protected?

There are various advanced Estate Planning methods for protecting your home from creditors and litigants, and they are surprisingly not difficult to accomplish or to manage.

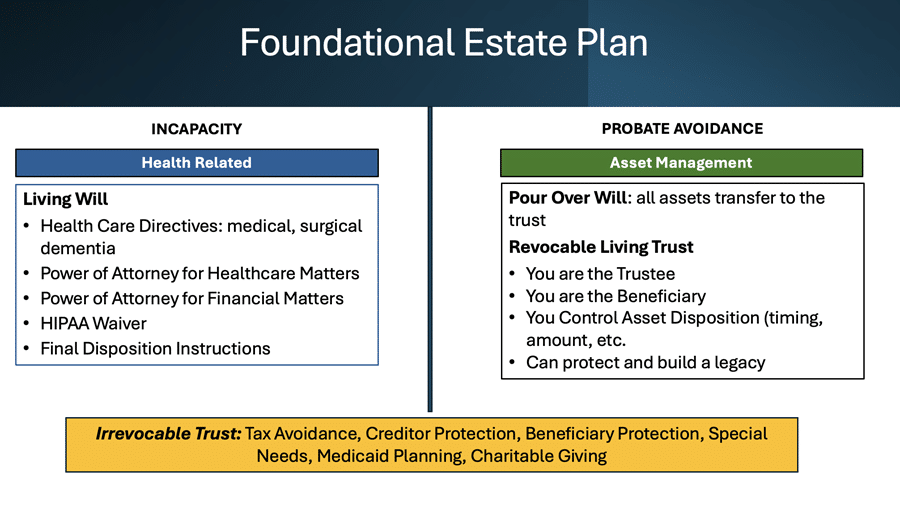

The only bullet proof method would be to remove your home entirely from your estate by placing it in an irrevocable trust. This option is not ideal if one is also wanting to preserve the tax benefits associated with a revocable living trust, including preserving your homestead exemption and the tax benefits of capital gains exclusion upon sale, step up in basis upon death, and the unlimited marital gift tax exemption.

The alternative is not bullet proof, for it does not ensure limited or no liability. Rather, it obfuscates the owner of record through a series of entities which creates a thick cloud of privacy making it very difficult for anyone to identify the true owner of your home.

Most litigators, especially those who work on a contingency fee (where they do not get paid unless they collect) do not want to spend a lot of money or time trying to work through the various obstacles. They tend to take cases in which they are confident they will be able to win and collect their fee. They look for people who have not taken the steps necessary to protect this precious asset.

This alternative solution includes a combination of entities including a Revocable Living Trust (which should be the foundation around which all your Estate Planning is built), a Real Estate Trust (also revocable), and possibly an LLC to function as a Trustee for the Real Estate Trust thereby ensuring your privacy as well as making it very difficult for someone to identify the asset as yours.

Then if your attorney is the agent of record, if anyone seeks information on the officers and members of the LLC, your attorney can claim Attorney Client Privilege thereby protecting your identity and the ownership of your home. And if they do find a way to identify the individual identity of the member(s) of the LLC, the LLC, acting as the Trustee of the Real Estate Trust, has a fiduciary responsibility to the beneficiaries of the Trust and not to the litigating attorney. Again, this makes it very difficult for a litigator to conduct effective discovery.

Are You Ready to Protect Your Home Like a Legacy Builder?

Life & Legacy Law can help you plan to protect your home from creditors and litigants, while preserving your homestead exemption and the tax benefits of capital gains exclusion on sales, step up in basis upon death, and the unlimited marital gift tax exemption. And of course, we can keep your estate out of Probate.

If you would like to discuss how we can protect you and your home, please contact me at 720-948-3553 or email me at steve@life-legacylaw.com. You can also go to the website: www.life-legacylaw.com and schedule a free consultation.

Stephen Villanueva,

Advisor and Personal Family Lawyer