How Relying On Beneficiary Designations Put Your Family at Risk (And How To Fix It!)

You’ve worked hard to build your assets and secure your family’s future. Like many responsible adults, you’ve named beneficiaries on your retirement accounts, life insurance policies, and maybe even your banking and investment accounts. It feels good to know you’ve put something in place for your loved ones.

While beneficiary designations serve a purpose, they’re not a comprehensive estate planning solution. Relying solely on them can lead to unintended consequences and potential financial disasters for your loved ones. Let’s delve into why beneficiary designations fall short and the risks you may unknowingly take with your family’s financial future.

The Dangers of Naming Minor Children As Your Beneficiaries

You love your children and want to ensure they’re cared for if something happens to you. Naming them as beneficiaries on your accounts is a straightforward way to achieve this goal. However, this approach can backfire spectacularly when your children are minors.

Designating a minor as a beneficiary creates a legal and financial predicament. Financial institutions cannot hand over large sums of money to children, so the court will likely appoint a guardian to manage the funds. This process can be time-consuming, expensive, and may not align with your wishes.

Even more concerning is what happens when your child reaches the age of majority, typically 18 or 21, depending on your state. At this point, they gain complete control of the inherited assets. Ask yourself: Is your 18-year-old ready to manage a six or seven-figure life insurance policy? What about your retirement account? For most young adults, the answer is a resounding no.

Imagine your child receiving a windfall at an age when they’re still learning to navigate adult responsibilities. They might make impulsive financial decisions, fall prey to manipulative friends or partners, or simply lack the maturity to handle sudden wealth. By relying solely on beneficiary designations, you’re potentially setting your child up for financial mismanagement or even exploitation. It’s a sobering thought that underscores the need for comprehensive planning.

When a Beneficiary Dies Before You

Life is unpredictable, and tragedy can strike at any time. While it’s uncomfortable to contemplate, your named beneficiaries may predecease you or die with you in an accident. This scenario can throw your estate into chaos if you’ve relied entirely on beneficiary forms.

When a named beneficiary dies before you, the fate of those assets becomes uncertain. Some accounts may have provisions for contingent beneficiaries, but many people neglect to name backups. In other cases, the asset may revert to your estate, potentially subjecting it to probate – a time-consuming and potentially expensive legal process you likely wanted to avoid by using beneficiary designations in the first place.

The situation becomes even more complex if you and your primary beneficiary die simultaneously or in quick succession. In such cases, determining the order of death can have significant implications for how your assets are distributed. Without a comprehensive estate plan, your assets may go to unintended recipients or get tied up in lengthy legal battles.

Establishing a will or trust can create a chain of inheritance that accounts for multiple contingencies, ensuring your assets are distributed according to your wishes regardless of the circumstances. This level of control and reassurance is a key benefit of comprehensive planning.

The Risks of “Set-It-and-Forget-It” Planning

Life is dynamic and filled with changes, both big and small. Your financial situation evolves, relationships shift, and laws change. Yet, all too often, people treat beneficiary designations as a “set it and forget it” solution. This static approach to estate planning can lead to severe problems.

- Consider how much can change over a few years or decades.

- You may divorce or remarry, dramatically altering your family structure.

- Children grow up, and your relationship with them may change.

- Your financial situation could improve significantly, making previous designations inadequate.

- Tax laws and regulations around inherited assets may be revised.

- You might develop new philanthropic interests or want to include charitable giving in your legacy.

If you don’t regularly review and update your beneficiary designations, they may no longer reflect your current wishes or circumstances. It’s not uncommon for people to unknowingly leave substantial assets to ex-spouses or estranged relatives simply because they failed to update their beneficiary forms.

In addition, beneficiary designations don’t allow for the nuanced distribution of assets that many people desire as their wealth grows. You should establish conditions for inheritance, protect assets from creditors, or provide for family members with special needs. These complex wishes simply can’t be accommodated through standard beneficiary forms.

The Peace of Mind That Comes From Careful Planning

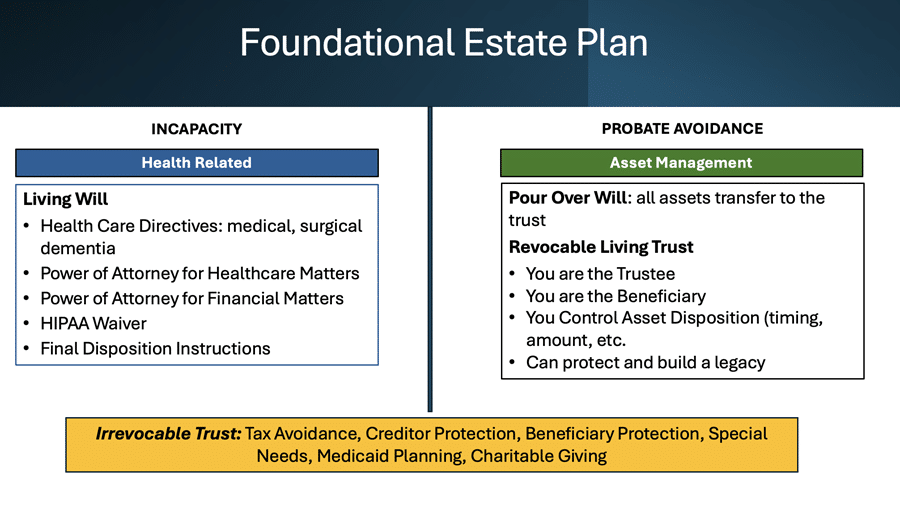

To truly protect your legacy and ensure your wishes are carried out, you need a Life & Legacy Plan rooted in education about what would happen to you, your family, and your assets if you become incapacitated and when you die. From there, we craft a plan that reflects your wishes, works when needed, and fits within your budget. This might include a will, one or more trusts, powers of attorney, healthcare directives, and carefully considered beneficiary designations. When we complete your original Life & Legacy Plan, you’ll have peace of mind knowing that it will:

- Protect minor beneficiaries and ensure assets are managed responsibly;

- Provide for multiple contingencies, including the death of beneficiaries;

- Minimize taxes and avoid probate when possible;

- Reflect your values and complex wishes for asset distribution;

- Adapt to changes in your life, finances, and the legal landscape.

Don’t leave your legacy to chance or expose your loved ones to unnecessary financial risks. Your family’s future security is worth the time and monetary investment in proper planning. Remember, a truly effective estate plan is a living document that grows and changes with you, providing peace of mind today and security for generations to come.

Know, too, that if you’ve already created your Life & Legacy Plan with me, keep an eye out for reminders to review and update your plan. If you know that you need to update your plan before we remind you, don’t hesitate to call us immediately.

Schedule a complimentary 15-minute consultation to learn more about how we support you.

Contact us today to get started.

This article is a service of Life & Legacy Law, a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning™ Session, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.