Celebrity Estate Plans Series Part 2 of 4: Vanilla Ice Has Thoughts

This week, we’re continuing to look at the lives of 4 celebrities and how they’re preparing for the inevitable (or didn’t!). Last week, we examined Michael Jackson’s planning and the holes in his plan that resulted in his family being embroiled in court and conflict for 15 years and counting (if you missed it, go back and check it out!) in this second article of our 4-part celebrity series, Vanilla Ice chimes in with his estate planning experience, advice, and lessons learned on a video he posted to his YouTube channel. He has a lot to say!

Vanilla Ice (Really) Hates Estate Taxes

Vanilla Ice shares the story of his buddy Mark, whose parents owned a sprawling property in Palm Beach, Florida. When they passed, Mark and his siblings sold the estate, expecting to be set for life. However, estate taxes ended up taking over 80% of their profit. Ouch.

Vanilla Ice calls this tax a “generational wealth killer,” he’s not wrong. Estate taxes can sneak up and bite a massive chunk of your wealth. And the thing is, with a proper estate plan, this doesn’t have to happen! The key is to educate yourself. Knowing what you’re up against helps you plan smarter so that more of your hard-earned assets reach your heirs.

Education is the most important part of estate planning. That’s why my planning process begins with a Life & Legacy Planning Session, where you’ll get the plain and straightforward education you need to make wise decisions about your planning, including how to keep your family out of court and out of conflict, minimize taxes, and ultimately create a plan that works for you and the people you love, when they need it.

So, first lesson: if you suspect your family could pay estate taxes at your death, don’t wait to plan. There’s way too much at stake. Call us, and let’s get you to know about the kind of planning you want and need for yourself and the people you love.

Vanilla Ice Thinks Life Insurance is Cool

(“Ice” and “cool” – get it? Sorry, I couldn’t resist.)

Life insurance isn’t just for covering funeral costs – it’s a secret weapon in estate planning. Vanilla Ice suggests “maxing out your life insurance” to give your kids as much money as possible. What makes life insurance “cool” is that death benefits aren’t subject to income tax, meaning your heirs can get more bang for your buck than if you were investing the money you’d put into life insurance premiums into just about any other asset class.

It’s worth considering what Vanilla Ice suggests here. When you take out a life insurance policy, the payout can cover any necessary taxes, probate fees, and debts, ensuring your heirs receive the lion’s share of your assets. Life insurance can help with short-term needs, like paying off a mortgage, or it can serve your family’s long-term needs, like maintaining the lifestyle to which they’re accustomed.

When you get educated via our Life & Legacy Planning process, we’ll look at your life insurance, whether you have the right amount and the right type, and ensure you are 100% clear on what it might mean to “max out your life insurance” and if you really should do that. We’ll consider whether you need more insurance, less insurance, or a different kind of insurance based on your family dynamics, assets, and what you want for the people you love after you leave.

Second lesson: If you want to be cool, plan to buy the right type and kind of life insurance.

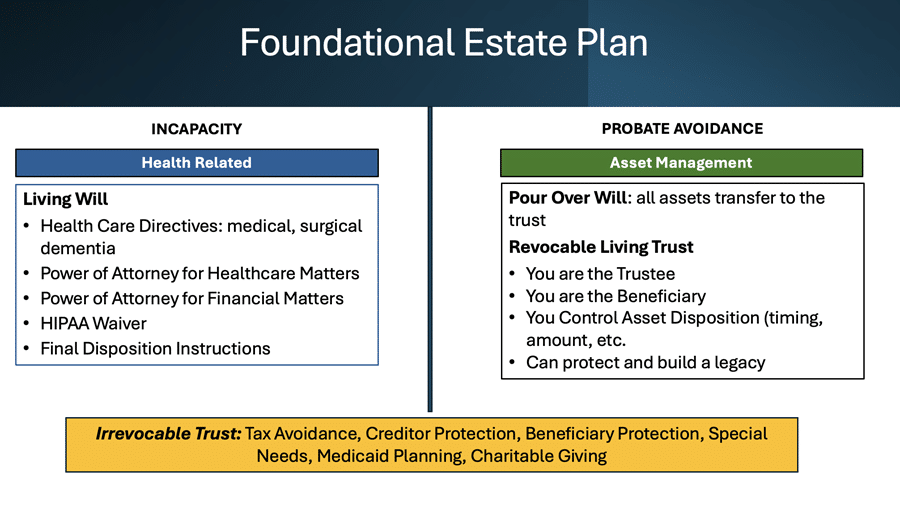

Ice Says Trusts Are Not Just for the Rich and Famous (and He’s Right!)

Trusts might sound like something only the super-wealthy need, but they’re an intelligent tool for anyone looking to protect their assets.

Ice mentions irrevocable trusts specifically. These types of trusts let you transfer assets to a beneficiary while removing the assets from your taxable estate, ensuring your assets aren’t subject to estate taxes. Any assets in an irrevocable trust are protected from legal judgments and creditors IF you do it correctly and in the right jurisdiction. If it’s something you are interested in, contact us, and we can talk. In the video, Ice jokes about putting his classic car collection into a trust and setting rules, such as his kids can lease but not sell the cars. This protection ensures your heirs benefit from it, but don’t squander the assets. In other words, even after death, you can determine how your assets will be used. And if you want to protect them for future generations, you can. This is one way to create generational wealth.

So now we’re up to our third and final lesson: If you want to protect and preserve your assets for generations, take Vanilla Ice’s advice and utilize trusts in your planning.

Put Vanilla Ice’s Advice Into Action Today

Vanilla Ice’s video brings forward lessons everyone can benefit from. By understanding your options, including how taxes and life insurance impact your family and assets specifically, and considering using well-counseled trusts, you can safeguard your assets and ensure they benefit your loved ones the way you want. To quote his classic hit, “Ice Ice Baby,” ‘Anything less than the best is a felony.’ Take these lessons from Vanilla Ice to heart, and start building a solid estate plan today. Your future generations will thank you for it.

We help you create a Life & Legacy Plan rooted in education and clarity so your loved ones stay out of court and conflict and your assets are protected. Once we’ve created your plan, you can rest easy knowing you’ve done the right things for the people you love most.

Contact us today to get started.

This article is a service of Life & Legacy Law, a Personal Family Lawyer® Firm. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That’s why we offer a Life & Legacy Planning™ Session, during which you will get more financially organized than you’ve ever been before and make all the best choices for the people you love.

The content is sourced from Personal Family Lawyer® for use by Personal Family Lawyer® firms, a source believed to be providing accurate information. This material was created for educational and informational purposes only and is not intended as ERISA, tax, legal, or investment advice. If you are seeking legal advice specific to your needs, such advice services must be obtained on your own separate from this educational material.